Our goal is for that impact to be truly global, and to make it easy for organizations everywhere to use our platform to build and scale their programs easily – without needing to worry about setting up their own connections to phone companies (telcos) or to middlemen (aggregators).

It’s practically impossible to connect directly to every telco in the world, so working through aggregators is necessary to have a truly global footprint. Some aggregators are country-specific or regional, while others are truly global. You may have heard of some of the global ones – Twilio is a global SMS and Voice aggregator; Nexmo is an SMS aggregator that is moving into Voice and USSD. You also may have heard of WorldText and Clickatell – both SMS aggregators. All of these also offer virtual phone numbers for some of their applications.

We’ve spoken in great detail with those companies any many many other national, regional, and global SMS and Voice aggregators. We’ve asked tough questions; we’ve probed to understand the industry. As soon as we heard about a term – like SS7 or grey route – from one company, we interrogated the others to find out more. We met industry insiders at conferences, and grilled them. After all of our research, we’ve come away with what we believe is a pretty thorough understanding of the industry, and we think our analysis is worth sharing, as transparency is one of our core principles.

In this article, we’ll focus on the SMS industry because the voice space has changed considerably and is a lot less opaque. The world of international SMS delivery, on the other hand, is still a very messy place.

A History of the SMS Aggregator Industry

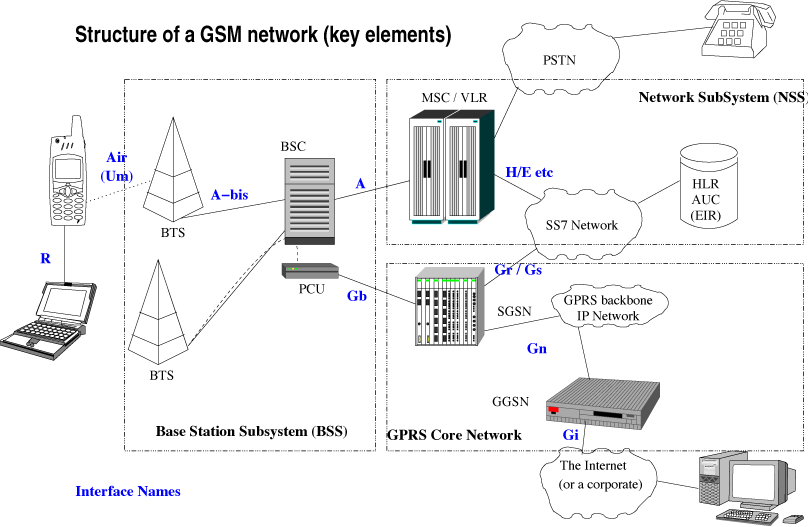

Let’s start with a little history lesson. When people started to travel internationally with their mobile phones, they wanted (needed) to be able to continue communicating via their mobile phones with their coworkers, friends, and family back home. The telcos quickly jumped on this and started building international roaming networks. They set up a global signaling system, called SS7 (Signaling System #7), to facilitate that person to person (P2P) traffic. In other words, SS7 allowed a Ugandan traveling in Poland to be able to send a text message from their Ugandan phone (containing their Ugandan SIM card) to their coworker back in Uganda and then to receive a response in Poland from that Ugandan coworker.

SS7 permits every telco in the world to reach every other telco in the world. Typically, one telco would charge another one for sending an SMS to their network. But because this system was designed to transmit P2P telecommunications traffic, most operators saw the traffic as balancing out and often didn’t charge the other telcos. For example, if Jane has a Telco 1 SIM card and sends an SMS to John who has a Telco 2 SIM card, Telco 1 will pay Telco 2 a fee for receiving and processing the SMS. But, because two real people are communicating, the telcos expect that John will reply to Jane’s SMS, thereby requiring Telco 2 to pay a fee to Telco 1. Because these fees essentially cancel each other out, the telcos often didn’t charge each other for sending SMS messages to each other’s networks.

The Rise of the Aggregators

But then something happened. Some aspiring entrepreneurs saw an opening in this SS7 world. First, they knew that to be able to send traffic on these SS7 roaming networks, a company needed to have a Global Title, which identified them as a network operator. Second, they knew that any telco would let traffic into their network so long as it was identified as coming from another telco, i.e., a company with a Global Title. And third, they knew that most telcos didn’t charge for incoming traffic because they expected that the traffic would be two-way, expecting the costs to balance out when the recipient on one network would send a reply to the sender on the other network. The telcos would then both earn fees locally from their customers without having to charge each other.

Getting a Global Title was also incredibly easy; it is so easy in one country that the industry refers to it as the brothel of the Global Title industry (I won’t name the country, but you can get a Global Title there in 30 minutes). The new companies that acquired Global Titles weren’t telcos in the traditional sense; they were aggregators. They didn’t have individual people as customers; they didn’t offer SIM cards; their customers didn’t have mobile phones. Instead, their customers were businesses that wanted to send out huge numbers of SMS messages to individual mobile phones for very cheap. These were one way messages from a computer application, what the industry refers to as application to person (A2P) traffic.

So many of these companies popped up that it became very difficult for true telcos to determine which Global Titles where sending P2P traffic and which were sending A2P traffic. And the problem with the A2P traffic was that it was one way, so the telcos receiving the messages didn’t have traffic going in the other direction, and the traffic thus wasn’t balancing out as it does with the P2P traffic. In short, the telcos weren’t earning anything from this A2P traffic; they weren’t charging for SMS messages coming into their network that they should have been charging for – and they were giving up on huge amounts of revenue.

Some of these third party companies, or aggregators, also started developing really bad reputations. A lot of the A2P traffic that they were sending was unsolicited bulk marketing messages, otherwise known as SPAM. Some also abused the direct connections they had with major telcos. Telcos would allow aggregators to pay a fee to have a direct connection to the telco’s network. If they have a direct connection, then they can send traffic through the telco’s network to anywhere in the world. Some aggregators sent so much A2P traffic through the networks of the telcos with which they had direct connections that recipient telcos started blocking traffic coming from those major telcos.

These SS7 networks – and the ease of jumping on them – was becoming a serious problem. There was so much SPAM running around the world that telcos got fed up with these companies abusing the SS7 signaling system. Aggregators were also bouncing traffic across each other to make it even harder for telcos to know whether the traffic was coming from another telco and was P2P traffic or was coming from an aggregator and was A2P traffic. The bounces are called “hops”; some aggregators would use many hops to pass an SMS to a mobile phone, which made a lot of the traffic cheaper but also decreased the likelihood that the message would actually make it to the recipient’s mobile phone. These routes became known as grey routes, and are generally regarded as unreliable. And on top of everything, the telcos weren’t happy that all this was money flowing around and they were seeing very little of it.

The Telcos Fight Back

{kind=link}

{kind=link}

Many telcos decided that they had to start blocking the grey routes. But, there was a problem. The telcos could only see what was coming into their network, not necessarily where it was coming from, so if they shut down a connection (i.e., didn’t allow traffic in from a particular SS7 route), then they might be blocking a non-grey roaming route and blocking P2P traffic, which was a big non-no. They started to work with aggregators they trusted to help the telcos figure out which routes were true grey routes and which were legitimate. The telcos then started shutting down a lot of the true grey routes and allowed certain aggregators to directly connect into their networks, thereby allowing all traffic passing through those directly-connected aggregators to get through to the telco’s network.

This “clean-up” process is currently in its infancy and it will have two big outcomes for businesses like ours and our customers – one positive and one negative outcome:

The Positive: International SMS traffic will become more reliable and more stable, as fewer grey routes will exist.

The Negative: SMS prices likely will go up a bit because telcos will start getting a cut of the action.

While researching the telecom industry, we came across a lot of new and fascinating information and thought we’d share what we learned with our readers. We’ll share more in future blog posts. In the meantime, if you have any questions about all of this, please let us know in the comments below – or if you’re an industry insider and you have a different understanding of these issues, please let us know in the comments as well.